“Give thanks in all circumstances; for this is the will of God in Christ Jesus for you.” 1 Thessalonians 5:18 ESV

Thanksgiving Holiday Schedules

The US Financial markets will be closed on Thursday, November 24th and will only be open for a half-day of trading on Friday, November 25th. Our office will close at 3:00pm on Wednesday, November 23rd and be closed on Thursday the 24th and Friday the 25th for Thanksgiving. Please remember this will delay any withdrawal requests from AXOS Advisor Services accounts by 2 extra days at the end of next week.

Mid-terms and Fed Hikes, Meh

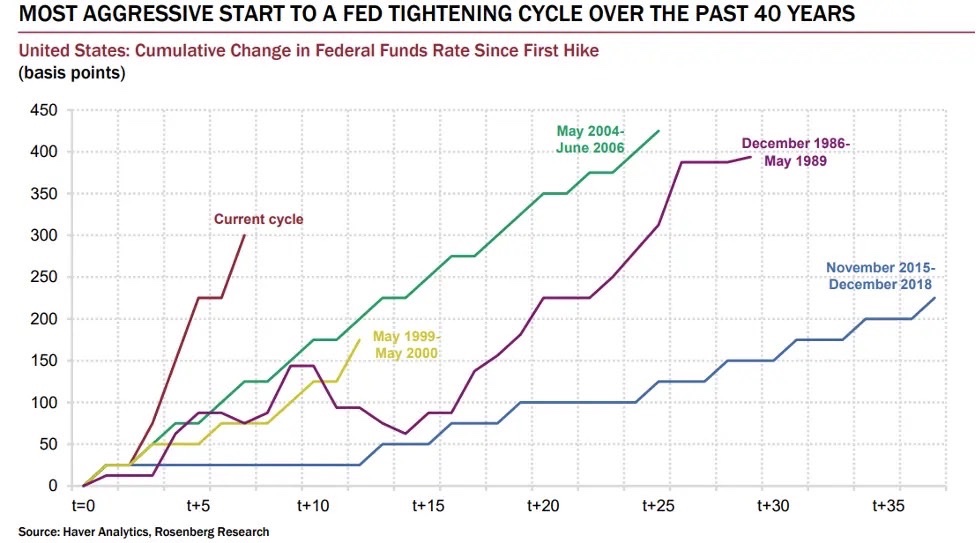

The Fed hiked rates an expected 75 basis points (.75) the first week of November, and the market surprisingly reacted with a sell-off. Since then, the October CPI number came out slightly more subdued than expected and led to a surge in equity prices. The market continues to act extremely sporadic with any slight change in data. We believe equity prices are attractive for long-term investors, regardless of any near-term domestic event. In our opinion, economic data previously relied on other market cycles is meaningless due to the repeated “ripples” we believe will be observed.

If the mid-terms lead to a split Congress, the markets could act favorably, as gridlock is always preferred due to more certain outcomes. However, if it does not occur, we still view equities as attractively priced. The Fed will almost certainly hike rates again in December, and the markets are sure to be volatile around the announcement on December 14th. The US economy remains strong with an extremely tight labor market, which will continue to motivate the Fed to hike rates. Our inflation fears have mostly subsided, with many commodities continuing to move lower, and higher rates could potentially lead to a slowdown in activity. The Fed has repeated its target for inflation at 2%, and it seems determined to get there regardless of the economic impact. As we’ve repeatedly said, the markets are not always linked to the economy, as markets are based on expectations and valuations.

Recession or Not

The graphic below shows a yield curve we typically pay close attention to that we’ve previously spoken about, the 10-year US treasury yield less the 3-month yield. As of last week, it had meaningfully fallen negative, which has previously led to a recession. While we believe this recession has seemingly already been priced in, it does not indicate what equity markets may do. It alerts us to the potential need for caution if the markets do not seem concerned. In this event, the markets are aware and witnessing depressed valuations. The indicator below can warrant caution in the fixed-income market as well. It is currently inverted and essentially the market saying it has concerns as investors are demanding more yield today than into the future. In a normal environment, investors are paid less today and given higher yields for longer-term bonds; hence, the market would indicate it is less concerned today than in the future. When this inverts as it is now, the market indicates it is worried. If valuations did not line up with this outlook, we would be more concerned.

We should also reiterate that recessions do not necessarily indicate equity/stock performance, as it all matters what the market has already “priced-in” and expects to occur. In our case, if a recession does materialize next year, equities could trade positively. From start to finish, the 1960, 1980, 1981, and 1990 recessions saw positive equity performances for the Standard &Poor’s 500 stock index.

Geopolitical Risks Remain Focus

Rather than the Fed’s actions or the mid-term results, our primary concern revolves around geopolitical risks. It is our opinion, and only an opinion, that Russia seems to be prolonging the war in Ukraine to the intentional detriment of Europe. We have taken actions to help hedge against this possibility, as Europe will face some extremely difficult times in 2023 if the war continues and power rates surge even higher. It’s anyone’s guess as to the military actions taken by various governments. Yet, many have expressed aggression, most notably, China towards Taiwan. If China were to pursue its efforts to reunite Taiwan with China, it could be assumed that the US would react as well, leading to further uncertainty and turmoil. We continue to monitor these risks, but we have said previously that war is a near constant. Another World War would surely increase volatility, but equities have remained a place to be invested during the first two.

FTX: A Classic “Bank Run”

Bank runs have been a thing of the past since the inception of the FDIC in 1933, following one of the most significant depressions America had ever seen. Before then, depositors with money in the bank could wake up with no savings if the bank failed. We believe this is one of the primary factors that made that depression so severe. Not only did customers lose their savings, but the deposits were destroyed for banks who would have lent out the funds and supported the economy. That is how banks function. No bank has all the money available as it does on deposit, but instead, very little as the majority of those funds are lent out. So, when every customer demands their money be withdrawn from the bank at once, it creates a run and typically leads to a collapse as banks do not have those funds readily available.

The customers who were unable to withdraw funds would have lost everything. However, since 1933, the banks must pay for FDIC insurance which has solved the specific issue of customers losing their deposits in the event of a bank failure. It took years, if not decades, to rebuild the entire financial system. A more recent bank failure that most Oklahoma clients remember was the collapse of Penn Square Bank in 1982. However, all insured depositors were made whole, and most of the economic reverberations were felt by the bust of the oil and gas industry, which could partially be pointed to as the beginning of the bank’s collapse. In an unrealistic world where oil prices soared forever, there may have never been a collapse.

Penn Square Bank was excessively concentrated in the energy industry. Additionally, the FDIC found the bank to have committed 451 criminal violations. Moreover, many of these loans were sold to out-of-state banks but serviced by Penn Square. A few larger banks took substantial losses from writing down Penn Square Bank’s loans they had purchased. This is like what many of us witnessed occur, except this time in the real estate industry, on a global scale during the 2008 financial crisis. And yet again, no insured depositor in the US banking system would lose funds during the Great Recession. Over a century, America has continued to develop a robust financial system with excessive protections granted to consumers. We typically favor deregulation. However, that comes from a stance of a heavily regulated market.

Today, cryptocurrency exchanges face little to no regulation, specifically international ones. It is essentially a step back to pre-1929 with no consumer protections. We previously warned against investing in cryptocurrencies in January 2021 and wondered why anyone in a developed country would throw away all their consumer protections to chase a line of computer code that we have no reasonable way of determining an intrinsic value. Since their highs, many of these cryptocurrencies have fallen substantially, with most losing almost all their value. The industry has been littered with fraud and schemes. Even the golden cryptocurrency, Bitcoin, has fallen nearly 75% from its high in 2021. Just like Penn Square Bank’s failure was most likely spurred by the severe drop in oil prices, we are also witnessing massive collapses in the crypto space potentially produced by the intense declines in these “assets.”

Most of you may have seen the headlines about FTX, one of the largest crypto exchanges, filing for bankruptcy. It is one of many bankruptcies in the space, but it will be felt more by consumers using their platform. Because just like in 1929, when no FDIC existed for bank depositors, no consumer protections existed in this exchange. A “bank run” potentially sparked by a competitor in addition to an industry witnessing severe price declines has led to FTX’s collapse and most customers potentially losing all of their deposits. FTX is now under criminal investigation as well as said to have used customer funds for its founder’s trading firm and mishandled funds.

While many won’t mourn the losses for Venture Capital firms, the amounts are piling up are material. Sequoia Capital wrote down their $213.5mm investment in the company. SoftBank is estimated to have about $100mm in exposure to the exchange. It should be noted that at the time of writing this, no F.I.G. client has any direct or known indirect exposure to FTX or the crypto industry in general for assets we manage.

We never understood how FTX existed in the first place, as their primary business was derivatives linked to cryptocurrencies. In general, derivatives are extremely volatile and challenging to brokerages due to their inherently leveraged nature. If you tie that to cryptocurrencies which have prices that are extremely volatile on their own, it seems extremely difficult to understand how any legitimate exchange could survive. Even more cracks are emerging now, as FTX had previously bailed out multiple entities in the industry this year. Another exchange, BockFi, just announced suspending withdrawals. Other exchanges seem to be helping competitors manipulate disclosures to try and curtail contagion. If the industry survives this event, the current moment will stand as a historical moment similar to 1929 for the financial sector.

While it is no surprise to clients, we recommend against “investing” in cryptocurrencies. We do not believe there would have been near the amount of interest if it were not for their meteoric bubble-like price, with Bitcoin now receiving the title of the fifth biggest wipeout of all time according to BofA. If its price decline continues, it could undoubtedly move up the list of historical bubble implosions. As value investors, we cannot value cryptocurrencies. Whether Bitcoin rises to $1,000,000 from here or continues to fall is anyone’s guess and not one we want to ever place our clients’ future financial well-being in. For client investments, we prefer traditional investment such as stocks and bonds for which we can determine some form of intrinsic value, knowing when it seems attractive to buy or sell.

We never like to witness excessive volatility like what has been seen this year in most investments. However, these moments typically bring the greatest amount of opportunity. So as we recently mentioned, we welcome clouds of economic uncertainty and maintain the view that the future is bright as we believe any economic clouds are eventually priced into stocks and will eventually clear given you are buying shares in businesses that are trying to grow and navigate any environment. As for the crypto industry, we have no idea what the future holds for it and whether its current “clouds” will ever dissipate. We have no desire to buy these digital assets “on the dip” and at lower prices, contrasted by us being enthused to see stocks go on sale that we believe can be effectively valued. In general, we prefer to be buying the dip in stocks when the opportunity arises and remember a major rule of investing: “Buy low, sell high”.

We wish you and yours a very Blessed Thanksgiving Holiday and may we take time to remember all we have to be thankful for this year. No doubt the last few years have been challenging in many ways, but we still have so much to give thanks for this year. We are so thankful for all of you and the privilege you have given us to be of service.

God Bless,

Your TEAM at F.I.G. Financial Advisory Services, Inc.

Uncertainty and Volatility